Home Equity Isn’t a Shortcut — It’s a Decision

For Sellers Kevin Baum April 1, 2026

For Sellers Kevin Baum April 1, 2026

Access to capital changes behavior.

Not because people become reckless — but because options expand. And when options expand, decisions become less about necessity and more about judgment.

Home equity is one of the clearest examples of this. It feels like found opportunity. But in practice, it’s simply repositioned leverage.

The question isn’t whether to use it.

It’s whether you understand what you’re trading.

Most homeowners don’t borrow against equity because they need to.

They do it because they can.

And that distinction matters.

Because once equity becomes accessible, it’s easy to frame decisions around possibility instead of outcome.

A meaningful portion of homeowners are tapping into equity — not for liquidity pressure, but for reinvestment into their homes and future positions.

The largest share is directed toward home improvements, with a smaller segment using equity to expand into additional real estate.

At a surface level, both decisions appear rational.

But they operate under very different assumptions.

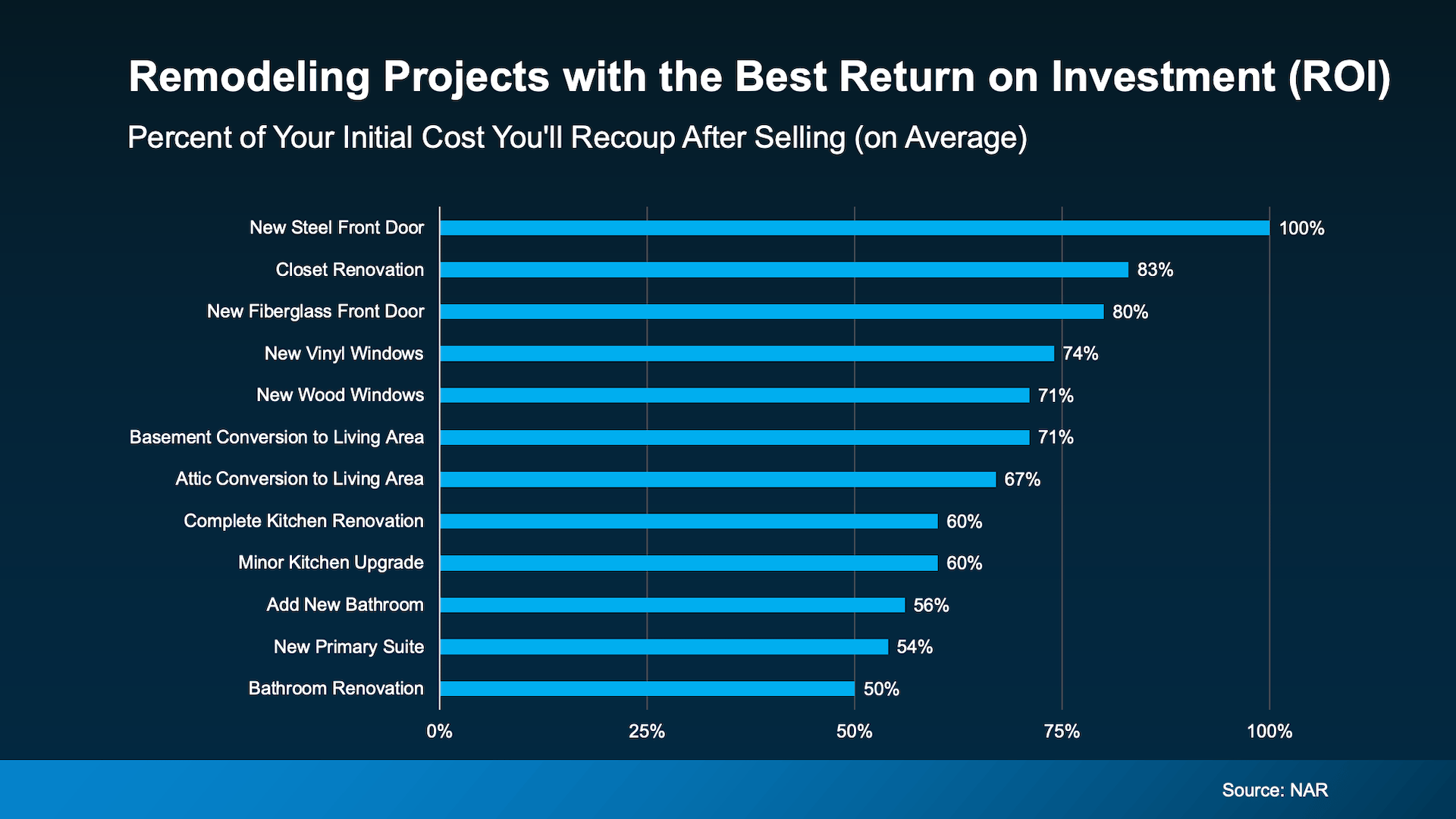

Using equity for home improvements is often framed as “adding value.”

But not all upgrades translate into market leverage.

Some improve lifestyle.

Some improve perception.

Very few directly improve pricing power.

The gap between those categories is where most homeowners lose clarity.

On the other hand, using equity to acquire additional property introduces a different kind of exposure.

Now the decision isn’t cosmetic — it’s structural.

You’re shifting from homeowner to investor, whether you intend to or not.

And that requires a completely different level of discipline.

Equity feels different than cash.

It doesn’t feel earned in the same way income does.

It feels accumulated.

And because of that, it’s often use with less resistance.

That’s where mistakes happen.

Not from poor intent — but from misaligned expectations.

A homeowner renovating a kitchen isn’t thinking about resale positioning.

They’re thinking about living better.

Which is valid.

But the market doesn’t price intention.

It prices outcome.

Equity should be treated as a strategic asset, not a convenience.

Before using it, three questions matter:

Because once equity is deployed, your margin for error narrows.

And in real estate, flexibility is often more valuable than optimization.

Clarity here doesn’t come from avoiding decisions.

It comes from understanding the role each decision plays.

And making sure it fits the position you’re trying to build.

Stay up to date on the latest real estate trends.

If this approach resonates, the next step is simple.